General Information

Disclosures on ESRS 2

The combined non-financial statement of Fraport provides information about the undertaking’s governance and performance in relation to substantial sustainability issues, including detailed performance indicators (sustainability indicators). The general information section contains identified material sustainability impacts, risks, and opportunities, as well as the principles of Fraport for the combined non-financial statement, which form the basis for its preparation.

Basis for Preparation

Disclosure Requirement BP-1 – General Basis for Preparation of Sustainability Statements

This combined non-financial statement is part of the 2024 management report and is prepared for the Fraport Group and Fraport AG in accordance with Section 315c in conjunction with Sections 289c to 289e of the German Commercial Code (HGB). The preparation was carried out with partial application of the European Sustainability Reporting Standards (ESRS) As a framework within the meaning of section 289d HGB. The aspects of the non-financial statement were integrated into the structure of the reporting, whereby the ESRS were partially applied.

| Aspects in the non-financial statement | Topics in ESRS |

|---|---|

| Environmental matters | ESRS E1 Climate change |

| ESRS E2 Pollution | |

| Employee-related matters | ESRS S1 Own workforce |

| Social Matters | ESRS S3 Affected communities |

| Customer satisfaction and product quality | ESRS S3 Affected communities |

| Respect for human rights | ESRS S1 Own workforce |

| ESRS S3 Affected communities | |

| Anti-corruption and bribery | ESRS G1 Business conduct |

The content of this report is based on a double materiality analysis (DMA), which was carried out in accordance with the ESRS requirements. The result of the analysis is that five out of ten ESRS topics are generally material for Fraport in the 2024 fiscal year. However, the content contained in this summarized non-financial statement does not fully reflect the result of the DMA due to the only partial application of ESRS. The following table shows the existence and scope of the ESRS disclosure requirements. “Partially applied” means a deviation from individual data points within the disclosure requirements. “Applied” refers to the full implementation of the ESRS disclosure requirements. “Not applied” refers to a disclosure requirement that is actually mandatory under ESRS, which is either derived from the DMA or is required independently of it as a minimum disclosure requirement, but is not reported. “Not material” describes a disclosure requirement that has been classified as non-reportable on the basis of the DMA.

| Disclosure requirement IRO-2 - Disclosure requirements included in the ESRS and covered by the company's sustainability statement | ||

|---|---|---|

| Reporting obligation | Description | Application status |

| ESRS 2-BP1 | General basis for preparation of sustainability statements | applied |

| ESRS 2-BP2 | Disclosures in relation to specific circumstances | partially applied |

| ESRS 2-GOV 1 | The role of the administrative, management and supervisory bodies | partially applied |

| ESRS 2-GOV 2 | Information provided to and sustainability matters addressed by the undertaking’s administrative, management and supervisory bodies | partially applied |

| ESRS 2-GOV 3 | Integration of sustainability-related performance in incentive schemes | partially applied |

| ESRS 2-GOV 4 | Statement on due diligence | partially applied |

| ESRS 2-GOV 5 | Risk management and internal controls over sustainability reporting | partially applied |

| ESRS 2-SBM 1 | Strategy, business model and value chain | partially applied |

| ESRS 2-SBM 2 | Interests and views of stakeholders | partially applied |

| ESRS 2-SBM 3 | Material impacts, risks and opportunities and their interaction with strategy and business model | applied |

| ESRS 2-IRO 1 | Description of the processes to identify and assess material impacts, risks and opportunities | applied |

| ESRS 2-IRO 2 | Disclosure requirements in ESRS covered by the undertaking’s sustainability statement | applied |

| ESRS E1 i.c.w. ESRS 2 GOV-3 | Integration of sustainability-related performance in incentive schemes | partially applied |

| ESRS E1-1 | Transition plan for climate change mitigation | partially applied |

| ESRS E1 SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | partially applied |

| ESRS E1 i.c.w. ESRS 2 IRO 1 | Description of the processes to identify and assess material climate-related impacts, risks and opportunities | partially applied |

| ESRS E1-2 | Policies related to climate change mitigation and adaptation | partially applied |

| ESRS E1-3 | Actions and resources in relation to climate change policies | partially applied |

| ESRS E1-4 | Targets related to climate change mitigation and adaptation | partially applied |

| ESRS E1-5 | Energy consumption and mix | applied |

| ESRS E1-6 | Gross Scopes 1, 2, 3 and Total GHG emissions | partially applied |

| ESRS E1-7 | GHG removals and GHG mitigation projects financed through carbon credits | not material |

| ESRS E1-8 | Internal carbon pricing | not material |

| ESRS E1-9 | Anticipated financial effects from material physical and transition risks and potential climate-related opportunities | not applied |

| ESRS E2 i.c.w. ESRS 2 IRO-1 | Description of the processes to identify and assess material pollution-related impacts, risks and opportunities | applied |

| ESRS E2-1 | Policies related to pollution | applied |

| ESRS E2-2 | Actions and resources related to pollution | applied |

| ESRS E2-3 | Targets related to pollution | partially applied |

| ESRS E2-4 | Pollution of air, water and soil | not material |

| ESRS E2-5 | Substances of concern and substances of very high concern | not material |

| ESRS E2-6 | Anticipated financial effects from pollution related impacts, risks and opportunities | not material |

| ESRS S1 i.c.w. ESRS 2 SBM-2 | Interests and views of stakeholders | applied |

| ESRS S1 i.c.w. ESRS 2 SBM-3 | Material impacts, risks and opportunities and their interaction with strategy and business model | partially applied |

| ESRS S1-1 | Policies related to own workforce | partially applied |

| ESRS S1-2 | Processes for engaging with own workers and workers’ representatives about impacts | partially applied |

| ESRS S1-3 | Processes to remediate negative impacts and channels for own workers to raise concerns | applied |

| ESRS S1-4 | Taking action on material impacts on own workforce, and approaches to mitigating material risks and pursuing material opportunities related to own workforce, and effectiveness of those actions | partially applied |

| ESRS S1-5 | Targets related to managing material negative impacts, advancing positive impacts, and managing material risks and opportunities | partially applied |

| ESRS S1-6 | Characteristics of the undertaking’s employees | applied |

| ESRS S1-7 | Characteristics of non employee workers in the undertaking’s own workforce | not material |

| ESRS S1-8 | Collective bargaining coverage and social dialogue | partially applied |

| ESRS S1-9 | Diversity metrics | applied |

| ESRS S1-10 | Adequate wages | not material |

| ESRS S1-11 | Social protection | not applied |

| ESRS S1-12 | Percentage of employees with disabilities | partially applied |

| ESRS S1-13 | Training and skills development | partially applied |

| ESRS S1-14 | Health and safety | partially applied |

| ESRS S1-15 | Work-life balance | not applied |

| ESRS S1-16 | Compensation metrics (pay gap and total compensation) | partially applied |

| ESRS S1-17 | Incidents, complaints and severe human rights impacts | applied |

| ESRS S3 i.c.w. ESRS 2 SBM-2 | Interests and views of stakeholders | applied |

| ESRS S3 i.c.w. ESRS 2 SBM-3 | Material impacts, risks and opportunities and their interaction of with strategy and business model | partially applied |

| ESRS S3-1 | Policies related to affected communities | partially applied |

| ESRS S3-2 | Processes for engaging with affected communities about impacts | applied |

| ESRS S3-3 | Processes to remediate negative impacts and channels for affected communities to raise concerns | applied |

| ESRS S3-4 | Taking action on material impacts, and approaches to mitigating material risks and pursuing material opportunities related to affected communities, and effectiveness of those actions and approaches | partially applied |

| ESRS S3-5 | Targets related to managing material negative impacts, advancing positive impacts, and managing material risks and opportunities | partially applied |

| ESRS G1 i.c.w. ESRS 2 GOV-1 | The role of the administrative, supervisory and management bodies | applied |

| ESRS G1 i.c.w. ESRS 2 IRO-1 | Description of the processes to identify and assess material impacts, risks and opportunities | applied |

| ESRS G1-1 | Corporate culture and business conduct policies and corporate culture | partially applied |

| ESRS G1-2 | Management of relationships with suppliers | not material |

| ESRS G1-3 | Prevention and detection of corruption and bribery | partially applied |

| ESRS G1-4 | Confirmed incidents of corruption or bribery | partially applied |

| ESRS G1-5 | Political influence and lobbying activities | not material |

| ESRS G1-6 | Payment practices | not material |

This combined non-financial statement was prepared on a consolidated basis and includes all consolidated undertakings of the Fraport Group in accordance with the scope of the consolidated financial statements. Unless otherwise stated, the quantitative data refer to this consolidated basis. The concepts and approaches outlined in this combined non-financial statement apply equally to Fraport AG.

The companies (parent companies and subsidiaries) included in the combined non-financial statement correspond to those included in the scope of consolidation in the consolidated financial statements. They are included in accordance with the principle of financial control. For the purposes of GHG accounting, it was also examined whether the principle of operational control applies to joint ventures, associates and other investments in the Fraport Group that are accounted for using the equity method. A two-stage analysis was carried out to determine operational control. It has shown that Fraport does not have operational control over joint ventures, associates and other investments for the 2024 reporting year. Therefore, non-financial data for these companies is only included in Scope 3 accounting.

In sustainability activities and the assessment of sustainability impacts, Fraport deals with its own business operations at the respective sites as well as the upstream and downstream value chain. The first stage of the upstream and downstream value chain (Tier 1) was included in the process of determining the substantial impacts, risks, and opportunities.

Fraport purchases products and services from numerous suppliers. The German Act on Corporate Due Diligence Obligations in Supply Chains applies in the upstream supply chain. In this context, Fraport is also aiming at or including the first stage of the supply chain.

In its combined non-financial statement, Fraport does not include information relating to intellectual property, know-how, or innovation results. Likewise, information on upcoming developments or matters that are still in negotiation stages is omitted.

Disclosures Based on Other Legal Regulations or Generally Accepted Bulletins Regarding Sustainability Reporting

According to the “Act to Supplement and Amend the Regulations for the Equal Participation of Women in Management Positions in the Private and Public Sector” (FüPoG II), Fraport must provide disclosures on the proportion of women in management positions.

Disclosures pursuant to Article 8 of Regulation 2020/852 (EU Taxonomy Regulation) are published in the environmental information (E1).

Disclosure Requirement BP-2 – Disclosures in Relation to Specific Circumstances

The combined non-financial statement covers the period from January 1, 2024 to December 31, 2024.

The combined non-financial statement includes estimates of data from the upstream and downstream value chain. The analysis of the value chain is predominantly based on the assessment of experts from the Fraport Group and is therefore subject to a certain degree of uncertainty. The data is validated internally by the quality assurance body; no further external validation is performed. Uncertainties in connection with estimates are explained below.

Uncertainties related to estimates are explained below.

Supply Mix of Energy

The breakdown of energy consumption by individual generation types is based on electricity labeling or information on the composition, which is not regularly available for the current reporting year. If required market-related data was not available in individual cases, the next best site-related data was used. Fraport considers the resulting uncertainties to be low.

GHG Emissions

All reported GHG emissions are based on activity data such as energy consumption or transportation services and activity-specific emission factors. In the absence of local or more specific factors, the current emission factors of the Department for Environment, Food & Rural Affairs (DEFRA) were applied. Since these are generally prepared for the British economy, the application to activities in other countries leads to uncertainties. These go beyond the basic uncertainties of emission factors underlying life cycle analyses. In addition, data from the International Energy Agency (IEA), the Federal Office of Economics and Export Control (BAFA) and the Global Warming Potential (GWP) were used. Fraport considers these uncertainties for the calculation of Scope 1 and 2 to be low.

The forecasts of potential future GHG emissions without reduction actions are subject to estimates and uncertainties as described in the financial management report. In the short-term forecast, they are low and increase too much up to the target forecast in 2045.

GHG Emissions Scope 3, Categories 1 and 2

Fraport calculates its procurement-related GHG emissions from the production of delivered products and the provision of services from the upstream value chain using a multi-regional input/output model from an external service provider by assigning the procurement volume to 65 economic sectors on a country-specific basis. Uncertainties arise from the clustering of the overall economy into only 65 sectors with different average emission factors as the best possible, but not exact, allocation of products and services to these sectors. The uncertainty is assessed as medium for the absolute value and as low for the evaluation of the time progression.

GHG Emissions Scope 3, Category 3

The activity data corresponds to the energy data for Scope 1 and 2. The emission factors used come from DEFRA. Fraport assesses the uncertainty as low.

Category 7 Activity Data and Category 11 Landside Traffic

The amount of travel to and from sites of Fraport is based on surveys of both employees and travelers. The survey results were not up-to-date for all sites, particularly among employees. In the event of missing results, the transportation mode mix was extrapolated based on the next best reference site. The assumptions for the transportation mode mix for the start and flow of air freight are based on internal experts. Fraport considers the uncertainty to be medium.

Aviation Activity Data in Category 11

Half-distance fuel consumption calculations are based on distances between destinations and our sites, as well as aircraft type and route-specific fuel consumption information from EUROCONTROL. The uncertainty is assessed as medium for the absolute value and as low for the evaluation of the time progression.

GHG Emissions of Minority Interests in Category 15

Minority interests without flight operations are assessed on the basis of their revenue on the basis of the model described in Scope 3, Categories 1 and 2.

In principle, the local GHG emissions balance is used for minority interests with flight operations. If there were no GHG emissions for the reporting year in accordance with Scope 1 and 2 at the time of publication, the data was extrapolated on the basis of the previous year’s GHG emissions and the traffic volume for the reporting year. Delhi Airport also collects its GHG emissions for a reporting period from April to March. Fraport is not aware of any significant events between the reporting periods that have a significant impact on the emissions balance.

For Scope 3 GHG emissions, if the calculation deviates from the half-distance method, the extrapolation was based on Fraport investments with a comparable business model and local traffic volume to ensure comparability of the category with the other categories.

Fraport considers the overall uncertainty of GHG emissions in Category 15 to be medium.

Estimates Related to the Calculation of Pay Differences

In calculating the gross hourly wages for men and women within the group, a working time of 39.3 hours per week was assumed for employees not covered by collective agreements, expatriates, and board members. Further estimation uncertainties are associated with the inclusion of special payments.

Governance

Disclosure Requirement GOV-1 – The Role of the Administrative, Management, and Supervisory Bodies

For Fraport, a responsible and transparent corporate governance and monitoring framework is the cornerstone for creating value and trust. In accordance with the statutory provisions, Fraport AG is subject to a “dual governance system,” which is achieved by the strict separation of personnel in the management and monitoring bodies (two-tier board).

The Executive Board manages the strategic and operational business at Frankfurt Airport as well as the national and international investments of Fraport AG, and the Supervisory Board supervises the Executive Board. The members of the Executive Board and the Supervisory Board work closely together in the interests of the company. The Executive Board usually meets every week and constitutes a quorum if at least half of its members participate in the meeting. Resolutions are adopted by a simple majority of all the participating members of the Executive Board. In the case of a tied vote, the chair holds the casting vote. The Executive Board reports to the Supervisory Board on all relevant matters of business development, corporate strategy, including sustainability issues, and possible risks in a regular, timely, and comprehensive manner.

The length of the appointment of the Executive Board members is geared toward the long term and is five years as a standard. The Executive Board of Fraport AG is comprised of five members: Dr. Stefan Schulte (Chairman), Anke Giesen, Julia Kranenberg, Dr. Pierre Dominique Prümm, and Prof. Matthias Zieschang.

The Supervisory Board of Fraport AG supervises the activities of the Executive Board. As a rule, the Supervisory Board meets four times a year. It is composed of an equal number of representatives of shareholders and employees and comprises 20 members as provided for in the company statutes. The ten shareholder representatives are elected by the AGM, and the ten employee representatives are elected by the employees in accordance with the provisions of the German Co-Determination Act (MitbestG) for five years. Both the representatives of the shareholders and the employees have a gender quota of at least 30% women and at least 30% men.

The Supervisory Board has formed committees to increase its efficiency and to prepare for Supervisory Board meetings. In the 2024 fiscal year, these were the following committees: “finance and audit committee,” “participation and investment committee,” “personnel committee,” “executive committee” (meeting only if necessary), committee pursuant to Section 27 of the German Co-Determination Act (MitbestG) or “mediation committee” (meeting only if necessary), and “nomination committee” (meeting only if necessary). The chairpersons of the committees provided regular reports at the next Supervisory Board meeting to the plenum of the Supervisory Board on the work of the committees. In individual appropriate cases and in accordance with law, decision-making powers of the Supervisory Board are granted to the committees.

The members of the Executive Board have the knowledge and experience necessary to conduct the business of Fraport properly. The members of the Supervisory Board have the knowledge and experience necessary to be able to perform their monitoring tasks properly. Relevant areas of competence include strategy development and implementation, IT and digitalization, risk management and accounting. The members of the Executive Board continuously update their knowledge in the relevant areas by participating in specialist events, presentations by consulting companies, and information from the specialist departments within the Group. This also applies to sustainability issues.

The members of the Supervisory Board submit their skills and acquired knowledge for monitoring sustainability matters in a declaration.

| Executive Board | Supervisory Board | |

|---|---|---|

| Number of executive members | 5 | 0 |

| Number of non-executive members | 0 | 20 |

| Percentage of independent board members | – | 50% |

| Gender diversity | Executive Board | Supervisory Board |

|---|---|---|

| Percentage of men | 60 | 65 |

| Percentage of women | 40 | 35 |

The Executive Board has established appropriate responsibilities, tasks, and structures within the Fraport Group in order to enable the achievement of the sustainability targets. Responsibility for the proper design of sustainability management lies with the full Executive Board. In addition, the respective Executive Directors are responsible for the sustainability issues within their area of responsibility. The central unit of Fraport AG Corporate Development and Sustainability, which is assigned to the department of the Chairman of the Executive Board, manages and coordinates the further development of sustainability activities and continuous updating of the DMA on behalf of the Executive Board. The definition and implementation of actions with regard to substantial impacts, risks, and opportunities is the responsibility of the relevant departments or Group companies.

The Supervisory Board of Fraport AG deals with sustainability issues in various committees with clearly defined responsibilities. The finance and audit committee monitors financial and sustainability-related reporting, while the executive committee takes sustainability matters into account in the targets and remuneration of the members of the Executive Board. The risk committee regularly reviews the substantial corporate risks, including sustainability risks, and assesses appropriate management strategies.

The Executive Board bears overall responsibility for strategic management, including the sustainability management. On a quarterly basis and on an ad-hoc basis, it reports to the Supervisory Board on substantial developments, actions, and risks. Reporting is done in a structured format with detailed information on financial, operational, and sustainability-related metrics. In addition, the risk committee receives quarterly reports on current risk assessments and risk mitigation actions.

Fraport uses an integrated risk management system to identify, assess, and manage impacts, risks, and opportunities. This includes risk analyses, internal audits, and regular reporting processes for reviewing defined actions. An internal control system (ICS) ensures that risks are continuously monitored. An escalation mechanism enables the timely reporting of critical risks to the Executive Board and the Supervisory Board.

Further process steps for governance, in particular for monitoring and controlling impacts, risks, and opportunities, will be further developed as part of the ongoing updating of the DMA. Additional actions and monitoring mechanisms will be implemented in the next two years.

It is planned to define further actions and targets with regard to material impacts, risks, and opportunities and the measurement of progress toward achieving these targets, as well as the definition of their monitoring by administrative, management, and supervisory bodies in 2025.

Disclosure Requirement GOV-2 – Information Provided to and Sustainability Matters Addressed by the Undertaking’s Administrative, Management, and Supervisory Bodies

The Chairman of the Executive Board was regularly informed of the interim results of the double materiality assessment (DMA) – procedures for collecting, identifying, and assessing the impacts, risks, and opportunities. An overview of the procedure and the final results were presented to the full Executive Board in November 2024. After examination, the Executive Board approved the results of the DMA. The Supervisory Board, represented by the finance and audit committee, was informed twice about the results in the fall of 2024. The finance and audit committee is responsible for monitoring the impacts, risks, and opportunities. The Supervisory Board commissioned Deloitte GmbH Wirtschaftsprüfungsgesellschaft to audit the combined non-financial statement.

Projects within Fraport AG that require a decision by the Executive Board are regulated in the rules of procedure for the Executive Board. Accordingly, the applying section must also assess the justification for the decision in the decision with regard to its impact on non-financial aspects. There is currently no standardized decision-making process for dealing with projects that have opposite economic and sustainability-related effects. In individual cases, the advantages and disadvantages of the decision as well as the effects on the sustainability matters are compared and weighed against each other.

Disclosure Requirement GOV-3 – Integration of Sustainability-Related Performance in Incentive Schemes

Executive Board remuneration at Fraport AG is set by the undertaking’s Supervisory Board upon the recommendation of its executive committee that it formed and is regularly reviewed for appropriateness. The remuneration system is designed to promote the long-term and sustainable development of the Fraport Group and includes both fixed and performance-related components. In order to support sustainable corporate development, non-financial components are also included in the measurement of performance remuneration.

In order to integrate non-financial and other qualitative performance criteria into the Executive Board remuneration system, as well as to assess the collective performance of the Executive Board as the overall executive body, the bonus includes a so-called “modifier” with a range of 0.9 to 1.1. The modifier assesses both the collective performance of the Executive Board as well as the target achievement of non-financial performance criteria. The modifier is defined on the basis of a predefined list of criteria, which also includes sustainability-related ESG targets. ESG targets can include the aspects of occupational health and safety, compliance, energy and environment, customer satisfaction, employee concerns, or corporate culture.

Two strategic corporate targets and one ESG target, each with a weighting of one third, were adopted for the 2024 fiscal year. The ESG target is to construct a large-scale photovoltaic installation along Runway 18 West. The target achievement is based on the start of construction and the completion date of the photovoltaic installation.

The share of variable remuneration, which depends on sustainability-related targets, was 3.0% in the reporting year.

The remuneration of the members of the Supervisory Board, who act as the supervisory body of the Executive Board, is based on the following principles. Each member of the Supervisory Board shall receive a fixed remuneration payable at the end of the fiscal year. The Chairman of the Supervisory Board receives three times the fixed remuneration, the Chairman of the finance and audit committee receives twice the fixed remuneration, and the Vice-Chairman of the Supervisory Board and the Chairmen of the other committees of the Supervisory Board each receive one and a half times the fixed remuneration. For their membership in committees, Supervisory Board members receive an additional, fixed remuneration per committee and fiscal year, but for a maximum of two committee memberships.

In addition, each member of the Supervisory Board receives attendance fees for all attendance at meetings of the Supervisory Board and its committees. In addition, expenses incurred and, if applicable, value added tax incurred on the remuneration and meeting fees are refunded. The remuneration of the Supervisory Board does not provide for variable remuneration based on the economic success of the undertaking or specific variable sustainability-related performance remuneration.

Disclosure Requirement GOV-4 – Statement on Due Diligence

The due diligence is implemented by all bodies and committees as part of their regular meetings and is not the subject of special meetings.

The following table shows the most important aspects and steps of the due diligence procedures in accordance with the reporting, with partial application of ESRS:

| Core elements of due diligence | Sections in the combined non-financial statement |

|---|---|

| a) Integrating due diligence into governance, strategy and business model | ESRS 2 GOV-2 ESRS 2 SBM-3 ESRS 2 GOV-3 |

| b) Involvement of affected stakeholders in all key due diligence steps | ESRS 2 SBM-2 ESRS 2 IRO-1 ESRS E1-4 ESRS E2 i.c.w. ESRS 2 IRO-1 ESRS E2-1 ESRS S1-1 ESRS S1-2 ESRS G1-1 |

| c) Identification and assessment of negative impacts | ESRS 2 SBM-3 ESRS 2-IRO 1 ESRS E1-1 ESRS E2 i.c.w. ESRS 2 IRO-1 |

| d) Measures to counter these negative impacts | ESRS E1-3 ESRS E2-2 ESRS S1-4 ESRS S3-4 ESRS G1-4 |

| e) Tracking and communicating the effectiveness of these efforts | ESRS E1-4 ESRS E2-3 |

Disclosure Requirement GOV-5 – Risk Management and Internal Controls over Sustainability Reporting

Fraport has implemented a Group-wide risk management system and a central internal control system (ICS). The central internal control system systematically identifies, controls, and monitors material process risks. The ICS is based on the COSO framework and serves as a central tool for monitoring and ensuring the adequacy and effectiveness of substantial operational processes.

A Control Self-Assessment (CSA) is conducted annually to assess the adequacy and effectiveness of the system and to continuously improve it. The target of this is to assess the appropriateness and effectiveness of the business process controls and to identify possible weaknesses in the processes at an early stage. The knowledge gained is incorporated directly into the further development of the ICS. The results of the CSA are presented annually in Executive Board meetings. In addition, the finance and audit committee of the Supervisory Board receives an annual report on the appropriateness and effectiveness of the central ICS.

Internal controls have also been implemented or are in the implementation phase in the area of sustainability reporting. In order to ensure a uniform procedure and consistent documentation, these actions will be fully integrated into the central ICS in the coming fiscal year. The identification and assessment of risks in this section was carried out in advance, with substantial threshold values being defined. These include, in particular, financial risks that relate to earnings and liquidity, as well as reputational risks with a probability of occurrence of more than 50%.

Particular attention is paid to reporting process risks that could cause the external or internal reporting to be erroneous and therefore do not reflect the actual situation of the undertaking. To minimize these risks, Fraport relies on various control mechanisms, in particular on ensuring high data quality, carrying out plausibility checks, and the principle of multiple control in data checking and consolidation.

The Group-wide risk management system of Fraport not only identifies and assesses risks but also manages, monitors, and reports them. Risk is understood to be a possible future development or an event that could have a negative impact on the achievement of operational, strategic, or sustainability-related targets. Non-financial risks may have a negative impact on the achievement of the environmental, sustainable, and social targets of Fraport.

The risk evaluation is conservative and the worst-case scenario is always used as a basis. A distinction is made between gross risk – i.e. the maximum possible negative impact before countermeasures – and net risk, which remains after the actions have been implemented. The evaluation is carried out according to the methods defined in the “risk and opportunities report.”

The results of the risk evaluation are directly incorporated into the following steps of risk management, monitoring, and reporting.

Strategy

Disclosure Requirement SBM-1 – Strategy, Business Model, and Value Chain

Significant Groups of Products and/or Services Offered

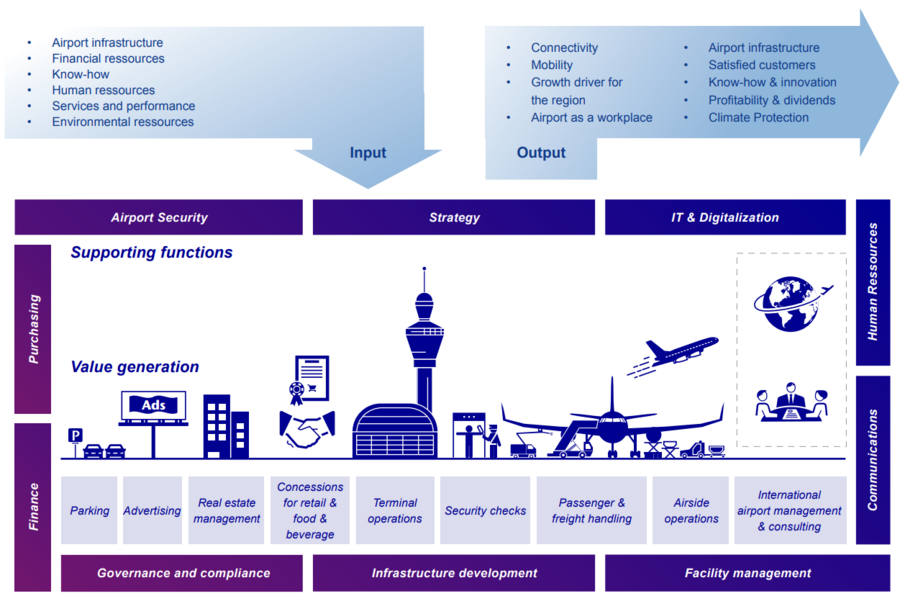

As an airport operator, Fraport provides a wide range of operational and administrative services for airport and terminal operations. Within the framework of the concession agreements, the scope of the services offered varies from contractually binding construction and expansion activities, administration and control of airport processes, to the management of retail areas. The range of tasks of the Fraport Group also includes planning and consulting services as well as IT services and facility management.

Fraport generates the majority of its revenue and earnings from the passenger and freight business at each of its sites. Fraport primarily levies charges for the use of the airport infrastructure, generates income from the development of commercial areas, and offers additional operational services. Fraport reports the main revenue streams resulting from this as “airport charges,” “infrastructure charges,” “ground services and security services,” “retail,” “real estate” and “parking.” In the area of airport concessions, revenue from “construction and expansion services in connection with IFRIC 12” are also reported. In its reporting, Fraport distinguishes between the following four segments:

- Aviation – holistic management of the terminal facilities and airport processes at Frankfurt Airport.

- Retail & Real Estate – development and renting of space at the airport and of space mainly near the airport in Frankfurt. This primarily includes the retail business, building and space leasing as well as parking management.

- Ground Handling – ground services such as loading, baggage and passenger services, as well as the operation of the central infrastructure and baggage transfer system at Frankfurt Airport.

- International Activities & Services – international marketing of the expertise of the Group and of airport operations as well as bundling central services in Frankfurt.

Fraport currently does not offer fully emission-free products or services. However, the business model includes individual economic activities that are classified as climate-friendly according to the EU taxonomy. As part of the decarbonization of our own business activities, the services offered are being made more sustainable. One indicator for such sustainable partial aspects is the taxonomy-aligned economic activities in the environmental target of climate change mitigation in accordance with the Delegated Regulation 2021/2178. Further details can be found in the section “Information on the EU Taxonomy Regulation.”

Significant Markets and/or Customer Groups

As an international airport Group, Fraport sees itself as a participant in the global aviation market in general. The focus of business activities is on the Group sites that are operated. In the segment reporting of the consolidated financial statements in accordance with IFRS 8, the sections of Germany, the rest of Europe, Asia, and the Americas form separately reported revenue regions.

Apart from passengers, its substantial customer groups especially include airlines, tenants of office and retail space, authorities, and freight forwarders.

The total number of employees in the Fraport Group was divided into the following geographical areas in 2024:

| Geographical areas | Number of employees |

|---|---|

| Germany | 17,010 |

| Europe (excluding Germany) | 1,962 |

| South America | 1,536 |

| North America | 64 |

| Rest | 18 |

| Total number of employees | 20,591 |

Breakdown of Total Revenue by Key ESRS Sectors

The consolidated financial statements of Fraport include segment reporting in accordance with IFRS 8. There is no breakdown of total revenue by ESRS sector.

Fraport is not active in the fossil fuel sector (coal, oil, and gas), in the production of chemicals, in the area of controversial weapons, or in the cultivation and production of tobacco.

Sustainability Targets

At the beginning of 2024, the new Fraport.2030 Group strategy was published. The sustainability targets of the Group are also anchored in this. The strategy includes the three strategic priorities: growth and sustainability, efficiency and innovation, and top employer. The first focus is on corporate responsibility and emphasizes that the growth-oriented Group strategy should not contradict sustainable action. The target of the strategic direction is to achieve long-term and profitable growth. At the same time, Fraport places a strong focus on sustainable aspects, in particular climate and environmental protection. In this context, Fraport is aiming for a position as the leading operator of environmentally friendly airports by 2030.

The strategic priority “top employer” includes capital expenditure of Fraport in the targeted training and further training of employees as well as the establishment of a modern HR organization. This strategic priority therefore also supports the taking of corporate responsibility as part of sustainability activities.

The progress in implementing the two strategic priorities mentioned above is measured using key performance indicators (KPIs). These include the number of passengers (in millions), GHG emissions (t CO₂e), and employee satisfaction. Quantitative targets have been defined for 2027 and 2030.

The strategy is implemented in all sections and companies of the Group by a selected and focused project portfolio. Projects with a particular communicative power were defined that support the rollout of the Group strategy and make it tangible (beacon projects). At the same time, the projects represent the Group’s core activities with regard to the long-term development of the company. Due to the broad concept of sustainability regarding social, economic, and ecological aspects, numerous strategic projects contribute to the strategic priorities “growth & sustainability” and “top employer.” The two projects “decarbonization master plan” and “HRneo” are to be highlighted here because of their high relevance in terms of content in the context of sustainability.

Decarbonization Master Plan

Because of the decarbonization master plan and the adopted actions, Fraport is committed to achieving net-zero status at the fully consolidated sites within Scopes 1 and 2. One of the most important actions of the master plan is the conversion of the electricity mix to renewable energies. This includes the undertaking’s own generation of renewable energies, energy storage, the development of an infrastructure for alternative drive systems, and the electrification of the vehicle fleet. Challenges in the implementation of the decarbonization master plan can arise from schedule and cost aspects. The availability of innovative technologies that can promote achievement of targets can also delay target achievement. Despite the challenges, no substantial adverse effects are currently expected in the course of the project.

HRneo

HRneo has the target of re-orienting the HR section and increasing the employer attractiveness of Fraport in order to position the undertaking for the future and to strengthen the cohesion of its workforce. The program includes targeted management development, the formulation of the new employer promise “Fraport. Your world of opportunities,” the establishment of specialized HR roles, and the further development of the HR organization. The results of the program were transferred to the line organization at the end of 2024 and form the basis for future-oriented modern human resources work. Change management, demographic change, intense competition for the best workers in an increasingly scarce labor market, and technical delays in implementation are the greatest challenges on the way to successful implementation of the project. Despite the challenges, we expect to successfully complete HRneo.

Disclosures of Inputs and Outputs

Fraport invests in the planning, construction, and maintenance of airport infrastructure such as runways, terminals, and parking garages. Operational airport management is another key element, which includes passenger and cargo handling, security controls, and baggage handling.

The most important economic players in the upstream and downstream value chain are in particular airlines, passengers, business partners in the real estate and ground services sector, concessionaires, and players in the cargo community. Their relationship is characterized by direct cooperation with the Fraport Group.

Fraport works closely with airlines to meet their needs, including ground handling and technical services. The commercial business, which includes retail, food services, and terminal services, contributes to customer satisfaction and additional earnings. The freight business is also considerable and includes comprehensive services for air freight, including storage and customs clearance. Facility management, which covers the maintenance and management of the airport infrastructure, relies on sustainable solutions to reduce costs and minimize environmental impact. Fraport pursues a customer-oriented and sustainable strategy to ensure economic success and to meet the requirements of the aviation industry.

In addition to finance, personnel, and environmental resources, the inputs of the business model also include the current infrastructure, existing know-how, and services from third-party providers. Using the “HRneo” and “decarbonization master plan” projects mentioned above, Fraport aims to secure personnel resources and reduce GHG emissions. The strategic targets "increase in EBITDA” and “free cash flow,” which are also included in the Fraport.2030 Group strategy, serve to maintain financial stability and provide the necessary financial resources for the further development of the Group – see the “Strategy” section.

The outputs of the business model include the connection of the respective regions in which Fraport is active to international markets (“connectivity”) and the associated mobility. Airports perform a public-service function. Because of their linking function across countries and continents, airports promote cultural interaction and international understanding.

The expansion and development of airports will increase capacities and attract additional passenger and freight traffic. This is accompanied by economic growth impulses for the regions around the airports, for construction, transportation and logistics, and later will also be accompanied by tourism and trade. Fraport contributes to economic prosperity. This is done within the Group, as a direct employer, indirectly at the respective airports and through industries that benefit from the added value of an airport, such as tourism (“growth engine of the regions” and “airport workplace”). Fraport also aims to achieve financially profitable growth for investors and sees itself as a good partner in the regions in which the undertaking operates.

As described above in the strategy and sustainability targets section, Fraport has set itself the targets of climate change mitigation and being a top employer and wants to inspire its customers with its airports and the services and products offered (know-how & innovations).

Disclosure Requirement SBM-2 – Interests and Views of Stakeholders

The main stakeholders of Fraport are its customers, business partners, owners, and employees. Their interests are reflected in the three strategic priorities of Fraport.2030. The relevant departments regularly seek their expertise on technical matters. By engaging with interests, Fraport wants to develop an understanding of the needs in relation to sustainability issues. Any stakeholder can contact sustainability management directly via the email address nachhhaltigkeitsmanagement@fraport.de.

Fraport has a broad network of institutionalized, structured communication media to promote dialog and a regular exchange of views. This includes forums for interaction with airlines, conducting regular surveys, and conducting systematic feedback management for passengers, employee surveys, investor conferences, interaction in airport associations, and especially for the Frankfurt site the Air Cargo Community Frankfurt, the Environment and Neighborhood House, and the Aircraft Noise Commission for continuous interaction with local authorities and citizens on topics relevant to airports.

Example of Neighborhood Dialog

The https://www.fraport.com/en.html website offers a wide range of services for residents living near Frankfurt Airport. Individual information on flight routes can be found on the interactive maps FRA.Map and FRA.NoM. The “My request” section provides the opportunity to provide feedback and to send inquiries to the neighborhood dialog team. There are also explanations on aircraft noise, actions such as noise abatement or roof protection programs, flight operations, or air quality. The impetus from this dialog will be used for the further development of actions for dealing with aircraft noise.

Example of an Employee Survey

The systematic exchange of information with the most important internal and external stakeholders enables Fraport to develop perspectives for the strategic alignment of the undertaking. The results of the employee survey are used to identify potential for improvement and derive appropriate actions. The results are used by the international Group companies to increase their own employee satisfaction. For the Frankfurt site, they are documented by the Central Unit “HRO,” which controls implementation and processes them for the sections or German Group companies. In individual cases, the actions and the intended improvements can be included in the target agreements with executives.

Example of an Owner

Consistent, timely, and transparent communication with the owners (investors) is very important to Fraport. The investor relations (IR) team of Fraport maintains face-to-face, telephone, and virtual contact with existing and potential investors as part of roadshows, capital market conferences, or regular meetings, including at the company headquarters at Frankfurt Airport. Over the past fiscal year, targeted individual and Group meetings again took place as well as presentations with the participation of the Chief Executive Officer, Chief Financial Officer, and Chief Infrastructure Officer.

Throughout the year, the IR team was available by phone (+49 69 690-74840) or by email (investor.relations@fraport.de) for direct dialog.

The telephone conferences for analysts on the financial publications, the AGM in May 2024, and the provision of up-to-date information on the IR website at www.meet-ir.com rounded off the range of IR services in the past fiscal year.

| Stakeholder | Engagement |

|---|---|

| Customers | Customer surveys |

| Business partners | Supplier code of conduct |

| Owners | Regular reporting, Annual General Meeting |

| Employees | Employee surveys |

| Neighborhood | Neighborhood dialogue |

| Society | Participation in associations |

Purpose of Inclusion

The impulses from the meetings referred to above are collected and reflected on by the responsible departments. The topics are reported to the Executive Board and Supervisory Board on an ad hoc basis. The inclusion of the interests of stakeholders/stakeholder groups can also serve to get to know their needs in relation to sustainability issues. These findings serve, among other things, to further develop sustainability activities in line with needs and thus increase the satisfaction of customers and employees, for example.

Disclosure Requirement SBM-3 – Material Impacts, Risks, and Opportunities and their Interaction with Strategy and Business Model

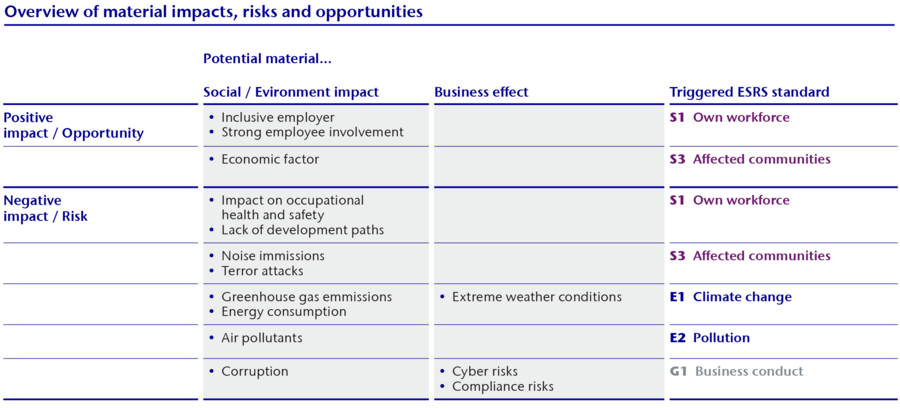

The following table provides an overview of the material impacts, risks, and opportunities in the Fraport Group:

| Disclosure requirement SBM-3 - Material impacts, risks and opportunities and their interaction with strategy and business model | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Description |

Impact, risk or opportunity |

Section in the business model/ value chain |

Influence on business model/ value chain |

Influence on strategy and decision-making |

Impacts on people and the environment |

Influence of strategy and business model |

Time horizon (short/medium/ long term) |

Direct (own activity) or indirect (business relationships) share of material impacts |

More information on actions in response to the current and expected impact | |

| E1 – Climate change | ||||||||||

| E1 – Climate change mitigation Greenhouse gas emissions (Scope 1, 2 and 3) |

The greenhouse gas emissions in Scope 1 and 2 are generated from the operation of the airport infrastructure and company vehicles. Scope 3 covers aircraft emissions during take-off and landing as well as passenger, freight, and employee traffic, and the supply chain. The negative impacts are dominated by the high emissions in Scope 3 | Negative impact |

The greenhouse gas emissions are generated during ground handling, flight operations, in terminal operation, and by the construction and maintenance of infrastructure. | low | medium | high | The greenhouse gas emissions are generated due to the business model. | Decreasing over the long term | Direct: in terminal operation, passenger and freight handling, and in flight operations indirect: at business partners |

Disclosure requirement E1-3 |

| E1 – Energy Energy consumption |

Airport operations require a high energy supply, in particular electricity for lighting and air conditioning as well as the operation of other technical systems. Depending on the site, there is also significant consumption of district heating and fossil fuels for the heating system and the vehicle fleet. The energy consumption of air transportation is also significant along the value chain. | Negative impact |

The energy is used in particular in ground handling, flight operations, terminal operations, and the operation of real estate. | low | medium | high | The energy consumption arises due to the business model. | Decreasing over the long term | Direct: in terminal operation, passenger and freight handling, flight operations, and by real estate management indirect: at business partners |

Disclosure requirement E1-3 |

| E1 – Climate change adaptation Extreme weather conditions |

Extreme weather conditions (e.g., heavy rain, heat waves, lightning, forest fires) lead to increased demands on the building infrastructure of airports. For example, system and control technology must withstand longer and hotter heat waves. In addition, extreme weather events such as heavy rain can cause operational interruptions at airports. Depending on the terms of the concession, this can lead to loss of revenue and unplanned additional expenses. | Risk | Extreme weather conditions can affect ground handling, flight operations, and terminal operation. | low | low | The evaluation of the risks from extreme weather events has not yet been completed. Due to the long observation periods, they are not currently taken into account in the risk and opportunities report. |

Disclosure requirement E1 and ESRS IRO-1 | |||

| E2 – Pollution | ||||||||||

| E2 – Pollution of air Air pollutants |

Air pollutants from flight operations include nitrogen oxides, carbon monoxide, particulate matter (PM10, PM2.5), hydrocarbons, ultra-fine particles (UFP), soot, and sulfur oxides. Research at Frankfurt Airport showed that during the COVID-19 pandemic, the reduction in low-level nitrogen oxide concentrations in the Rhine-Main region was primarily due to the decline in road traffic. For UFP, by contrast, flight operations are an important source and lead to increased concentrations around the airport. Due to their small size, UFP is classified as potentially hazardous to health, but due to a lack of epidemiological studies there is no dose-response relationship or limit value. Measurements at Group airports have not yet been required by law. | Negative impact |

Air pollutants are generated primarily during ground handling and near-ground flight operations. | low | medium | medium | The air pollutants arise due to the business model. | Decreasing over the long term | Direct: in passenger and freight handling and flight operations indirect: at business partners |

Disclosure requirement E2-2 |

| Disclosure requirement SBM-3 - Material impacts, risks and opportunities and their interaction with strategy and business model | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Description |

Impact, risk or opportunity |

Section in the business model/ value chain |

Influence on business model/ value chain |

Influence on strategy and decision-making |

Impacts on people and the environment |

Influence of strategy and business model |

Time horizon (short/medium/ long term) |

Direct (own activity) or indirect (business relationships) share of material impacts |

More information on actions in response to the current and expected impact | |

| S1 – Own workforce | ||||||||||

| S1 – Equal treatment and opportunities for all Integrative employer |

Fraport acts as an integrative employer and thus has a positive effect on people and society by its associated role model function. The Group promotes diversity and inclusion and, as a signatory to the Diversity Charter, actively communicates its values. In addition, Fraport offers jobs with low educational requirements, enabling people who have a difficult time gaining a foothold in other sectors of the economy to participate independently. | Positive impact |

The positive impact as an inclusive employer primarily comes from the company’s own operations. | low | medium | high | Inclusion and diversity are promoted by the HR strategy. Jobs with low educational requirements are created due to the business model. | Consistent over the long term | Direct: in all sections of the value chain where the undertaking’s own employees are utilized. (Not for concessions and not in flight operations) |

Disclosure requirement S1-4 |

| S1 – Social dialogue Strong employee participation |

Employees at the Frankfurt site in particular are represented Group-wide by representatives and trade unions. German co-determination requirements are being implemented at a high level. As a result, lower-wage employees in particular have a strong voice toward management, resulting in improved working conditions, higher wages, social benefits, and a high level of job security. The different groups promote participation and an understanding of democracy. At present, this impact is particularly pronounced in Germany. | Positive impact |

The strong employee participation takes place in the company’s own operations, particularly in Germany. | low | medium | high | Strong employee participation is also a result of the legislation and is only a limited result of the business model. | Consistent over the long term | Direct: in all sections of the value chain where the undertaking’s own employees are utilized. (Not for concessions and not in flight operations) |

Disclosure requirement S1-4 |

| S1 – Health and safety Impacts on occupational health and safety (physical and mental stress) |

Working conditions can be physically and mentally challenging, especially for different groups of employees on the apron and in the terminals for practical and organizational reasons. The existing initiatives to improve workplace resources, provide support and advice, and make work and working time more flexible are in principle helping to reduce negative impacts, but in some individual cases they are not yet sufficient. | Negative impact |

The physical and mental stress of employees arises primarily in the company itself, in addition to third parties whose employees work in the same sections. Terminal operation and ground handling are particularly affected. | low | medium | very high | The strong, especially physical strain, primarily during ground handling arises due to the business model. | Decreasing over the long term | Direct: in terminal operation, security checks, and passenger and freight handling indirect: for business partners |

Disclosure requirement S1-4 |

| S1 – Training and skills development Lack of development paths |

The lack of standardized career paths and opportunities for personal development impair employee motivation and long-term qualification for their future professional life in the sense of lifelong learning. Remedial measures are planned in particular through the HRneo strategic program and have already been partially implemented. |

Negative impact | Skills development takes place predominantly in the company itself. | low | medium | medium | Skills development is promoted by the HR strategy (HRneo). | Consistent over the long term | Direct: in all sections of the value chain where the undertaking’s own employees are utilized. (Not for concessions and not in flight operations) | Disclosure requirement S1-4 |

| S3 – Affected communities | ||||||||||

| S3 – Communities’ economic, social and cultural rights Economic factor (socio-economic contribution in the regions |

Expansion and development of airports increase capacity and attract additional passenger traffic and air freight. This is accompanied by economic growth impulses for the regions around the airports for construction, transportation, and logistics, and later also tourism and retail. In addition, airports have a role to play in providing public services. The linking function across countries and continents promotes cultural interaction and understanding. | Positive impact |

The socio-economic contribution in the regions is generated through interaction across the entire value chain. | low | low | high | The business model promotes the movement of people and goods in the regions and thus provides economic growth impulses. |

Consistent over the long term | Direct: across the entire value chain indirect: through business partners |

Disclosure requirement S3-4 |

| S3 – Adequate housing Noise immissions to residents |

Noise pollution is a negative impact of any airport on the people in the immediate vicinity. Exposure to aircraft noise was also assessed in the course of the planning approval notice for the expansion of Frankfurt Airport. The decision contains many specifications for limiting noise pollution. They are monitored annually to ensure compliance. In addition, programs for active and passive noise abatement have been implemented. Internationally, measurement obligations and perceived impact vary greatly but are generally much less pronounced. New types of ever quieter aircraft are counteracting projected traffic growth. | Negative impact |

Noise immissions arise from flight operations. | low | low | medium | The noise immissions arise due to the business model. |

Decreasing over the long term | Indirect: from flight operations | Disclosure requirement S3-4 |

| S3 – Security-related impacts Airport accidents/ terrorist attacks |

Proximity to airports increases the risk of people being affected by accidents or terrorist attacks. Fraport has therefore established a comprehensive preventive Safety Management System and Airport Security Management. The potential negative impact is high due to possible, serious accidents involving deaths or contamination. Safety measures can be used to prevent the probability and extent of negative impacts. The probability of a terrorist attack was set to very low in the risk aggregation. |

Potential negative impact |

Airport accidents and terrorist attacks can potentially be primarily related to terminal operation, ground handling, and flight operations. | low | medium | very high (The potential impact is high. Preventive actions reduce the probability.) |

The impact itself is not based on the business model. |

consistent over the long term | direct: from terminal operation, passenger and freight handling, and flight operations indirect: from business partners |

Disclosure requirement S3-4 |

| Disclosure requirement SBM-3 - Material impacts, risks and opportunities and their interaction with strategy and business model | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Description |

Impact, risk or opportunity |

Section in the business model/ value chain |

Influence on business model/ value chain |

Influence on strategy and decision-making |

Impacts on people and the environment |

Influence of strategy and business model |

Time horizon (short/medium/ long term) |

Direct (own activity) or indirect (business relationships) share of material impacts |

More information on actions in response to the current and expected impact | |

| G1 – Business conduct | ||||||||||

| G1 – Corruption and bribery Corruption |

Major projects at airports are mostly in the public light since they are flagship projects. That is why corruption cases have a very negative impact on undertakings, employees, and business partners. Corruption can occur both within the Group and at suppliers. Historically, investigations have already been carried out in isolated cases. Fraport is also active internationally in countries with a high risk of corruption. Occasional cases can be prevented by means of information and governance. In spite of various measures to prevent corruption, isolated cases with clear criminal intent cannot be prevented. | Potential negative impact |

Corruption can potentially occur throughout the value chain. | low | medium | high (the potential impact is high. The probability is low due to preventive measures). |

Airport development projects with large numbers of contracts provide the possibility of corruption in principle. The impact itself is not based on the business model. |

consistent over the long term | direct: potentially throughout the entire value chain indirect: from business partners |

Disclosure requirement G1, risk and opportunities report |

| G1 – Business conduct Cyber risks |

Cyber risks include cyberattacks, computer viruses, or hacker attacks that can cause serious business interruption due to a severe IT system failure or substantial data loss. An increased number of warnings from the German Federal Office for Information Security shows the rise in the threat situation. The strategy includes cyber insurance and extensive organizational/technical actions. | Risk | Cyber risks affect the entire business model and have potential impacts on the value chain. | high | medium | Low since it is classified as a financial risk |

Not specified since it is classified as a financial risk | gross increasing in the long term | Not specified since it is classified as a financial risk | Disclosure requirement G1, risk and opportunities report |

| G1 – Business conduct Legal and compliance risks |

Legal and compliance risks arise from changes in national and international laws and regulations, and violations of laws and regulations with a negative financial impact. For example, changes in aviation law, the German Federal Police Act, planning and environmental law, security-related regulations, general regulations under capital market law, antitrust law, data protection law, and labor law as well as any legal restrictions under sanctions, corruption, fraud, or financial manipulation, and antitrust violations. |

Risk | Legal and compliance risks have impacts on the business model and also on the value chain, depending on the type of change to national and international laws and regulations. | medium | high | Low since it is classified as a financial risk |

Not specified since it is classified as a financial risk | consistent over the long term | Not specified since it is classified as a financial risk | Disclosure requirement G1, risk and opportunities report |

In principle, no fundamental differences were found in the assessment of the material impacts, risks, and opportunities between Fraport AG and the Group. The positive impact of “strong employee participation” is only limited to the site in Germany due to the locally differing legal provisions.

The transformation of business and society into more sustainability is expected to intensify the innovation potential for new technologies and ways of working, such as automation and digitalization. Fraport is continuously looking for ways to mitigate its negative impacts, increase its positive impacts, compensate for risks, and thus refine its strategy and business model with the help of these new technologies and ways of working. In addition, Fraport will open up new business opportunities where possible with products and services that make a positive contribution to greater sustainability.

Further explanations on the material impacts, risks, and opportunities are contained in the respective topic standards.

Where actions have already been defined as a response to the current and expected impact of the material impacts, risks, and opportunities, a more detailed description can be found in the respective topic standard.

The material opportunities and risks arising from the IRO analysis and the associated potential impacts on the financial position, financial performance, and cash flows can be found in the assessments in the “Risk and Opportunities Report” section if the opportunity and risk thresholds are exceeded.

The material opportunities and risks from the IRO analysis are largely taken up in the two strategic directions of “growth & sustainability” and “top employer.” As explained in disclosure requirement SBM-1 the strategic directions are underpinned by targeted strategic projects. They are used, among other things, to exploit the opportunities resulting from the IRO analysis for Fraport and to reduce the identified risks.

The topics “noise immissions to residents” and “economic factor,” which are reported in the topic standard S3 Affected communities, and the cyber risks, which are explained in the context of G1 Business conduct, are provided by the undertaking as additional undertaking-specific information.

Impact, Risk and Opportunity Management

Disclosure Requirement IRO-1 – Description of the Processes to Identify and Assess Material Impacts, Risks, and Opportunities

Materiality Assessment Process

The analysis of double materiality was carried out for the Fraport Group in 2024. The target was to identify and confirm the material actual and potential positive and negative impacts, risks, and opportunities (IROs). They served as the basis for the Group’s decision on the substantial sustainability issues, which led to a double materiality assessment (DMA). The requirements of the ESRS were observed.

The DMA procedure was carried out for the first time, so there are no historical comparative values. The Executive Board has commissioned the Corporate Development and Sustainability department to define a process for the continuous updating of the DMA. Until the next review, the impacts, risks, and opportunities should be continually adjusted to business changes to ensure relevance and accuracy.

The process began with a comprehensive inventory of the potential issues as a long list that may be of importance to Fraport and its stakeholders to identify relevant sustainability issues in accordance with ESRS 1, paragraph AR16. In addition to the requirements of the ESRS, other sustainability matters such as the UN’s Sustainable Development Goals were taken into account in the collection of topics. The impacts on human rights was also taken into account. The process mentioned above was led by an expert committee.

Composition of the Expert Committee

The materiality assessment was carried out by an expert committee composed of members of various specialist departments and representatives of the Group companies. The value chain of the undertaking was represented in the expert committee. The committee bundled individual specialist knowledge from different sections of the undertaking with the target of a comprehensive and well-founded analysis.

Taking into account the business model and the scope of the consolidation as described in SBM-3, specific activities within the organization and business relationships in the upstream and downstream value chain were analyzed. This includes the actors in the value chain and the allocation of their impacts on the undertaking and the environment in the Group. Geographical conditions and other factors that could lead to an increased risk of negative impacts were also considered.

During the discussions, the Frankfurt site served as a model for the evaluation of the topics. The results were checked for plausibility by representatives of the Group companies for the entire Group and supplemented if necessary.

In the context of the expert workshops, the impacts of both the undertaking’s own activities and the business relationships within the Group were qualitatively evaluated. This provided a differentiated view of the direct and indirect impacts of the undertaking.

Consultation with Stakeholders and Internal/external Experts

Stakeholder involvement was determined using an web-based stakeholder dialog. 21 stakeholder groups, including employees and their representatives, passengers, airlines, suppliers and service providers, residents, shareholders, authorities, analysts, media, banks, NGOs, and associations have been grouped into four categories: employees, customers and business partners, owners, and society. The online survey was conducted in eight languages Group-wide and communicated via various channels (Internet, Intranet, LinkedIn, X (Twitter), press release, passenger interviews, letters to officials, emails to personal contacts, and much more). The results of the consultation were included in the discussions and evaluations within the subsequent workshops.

In the course of the workshops, the concerns of stakeholders were also represented by internal experts. The participants came from the respective departments of Fraport AG and have in-depth knowledge of their sustainability topics in order to assess the IROs and to contribute to taking into account the undertaking’s due diligence obligations. During the discussions, the Frankfurt site once again served as a model for the evaluation of the topics. The results were checked accordingly for plausibility by representatives of the Group companies for the entire Group and supplemented if necessary.

All sustainability issues were reviewed with the designated experts, with the focus on identifying IROs at the level of the undertaking. Financial materiality was also assessed separately with the involvement of the Executive Board. The process for determining the material impacts, risks, and opportunities was based on a combination of qualitative and quantitative methods, taking into account both the short- and long-term impacts on the undertaking and its stakeholders.

Decision-making During the Workshop

The evaluation of the impacts, risks, and opportunities was made within the expert group during the workshops. This process was based on an intensive discussion and analysis of the various aspects.

The decision-making process was based on the information gathered in the workshop, using a combination of qualitative and quantitative approaches. External studies were not explicitly used in the workshops during the discussion. After the initial identification of impacts, risks, and opportunities, a number of topics with similar content were summarized. All the IROs were evaluated in detail.

Identification and Evaluation of the Impacts, Risks, and Opportunities

All actual or potential positive or negative impacts, risks, and opportunities that the undertaking has on people and the environment, including its own business activities and the upstream and downstream value chain, were discussed. The impacts were then assessed in terms of scale, scope, and recoverability.

In terms of scale, the size or intensity of an impact was evaluated on a scale of 1 to 4 (minimum; medium; high; very high). Where comparison with a similar industry was possible (for example, with other undertakings in the transportation and logistics sector), they were used as a benchmark. The scope was also evaluated on a scale of 1 to 4 based on the range or spectrum of impact. The immutability, which was evaluated only for negative impacts, is defined as the ability to undo or mitigate the impact. It was also classified on the same scale.

For the risks and opportunities, the assessment was derived from the procedure in risk management. The gross assessment was carried out. The risks and opportunities were classified on a scale of 1 to 4 (minimal; noticeable; impact on business activities; high losses) with regard to the scale of the monetary and media impact. The probability was evaluated in gradations of 0.2 in increments of 0.2 to 0.8 (unlikely; possible; likely; very likely). A net assessment was also carried out in accordance with risk management.

The following short, medium, and long-term time horizons have been defined for the assessment of the material impacts, risks, and opportunities: The short-term view covers one to two years, the medium-term is a period of two to five years, and the long-term is a time horizon of five to ten years. The time periods defined in this way differ in the short-term view from the time horizons according to ESRS 1. This is related to the continuity and consistency with the time taken into account in the risk and opportunity report. Longer periods were considered when assessing climate risks. For more information, see the disclosure requirement ESRS E1 Climate Change.

Fraport attaches great importance to respect for and promotion of human rights along the entire value chain. As part of the ESRS, human rights aspects are considered and evaluated separately in order to ensure that they are an integral part of the sustainability strategy. The material impacts, risks, and opportunities in the area of human rights will always be included in the calculations as actual IROs. This ensures precise recognition and consideration of human rights issues in the reporting and contributes to transparent and responsible corporate governance.

Determination of the Threshold Value and Prioritization

The threshold value and the determination of the materiality for reporting correspond to the requirements in risk management based on probabilities and final evaluation (see report matrix in the management report, section: Risk and Opportunities Report), provided that ESRS rules do not conflict with them.

All issues that exceeded the threshold were highlighted and discussed in detail in the report in accordance with the ESRS.

Input Parameters Used

The data and information for the analysis come directly from the specialist departments. The practical data sources provided a realistic and relevant basis for assessing the identified risks and opportunities. Examples of such data sources include information on compliance with environmental pollutant thresholds, supply chain facts provided by Purchasing, and other specific information from various business units. Finally, the assessments of the risks in the risk inventory of Fraport were used by means of the risk reports.

Application in the Undertaking

Fraport AG has used the above procedure to create a sound basis for determining the disclosures in its sustainability statement. In the future, the results of the procedure will be regularly reviewed to ensure that the evaluations are accurate and up-to-date.

As described above, the Frankfurt site served as an example of a model for the evaluation of the topics. The results were checked accordingly for plausibility by representatives of the Group companies for the entire Group and supplemented if necessary.

The risk and opportunity management procedure is explained in detail in the “Risk and Opportunities Report” section. The thresholds value for the evaluation and classification of sustainability risks, which could have financial impacts on the Fraport Group, are applied in the same way as for other risk types.

Final Evaluation

From the individual assessments for scale, scope, and immutability, the maximum value is used for the overall assessment of the severity of each positive or negative impact. For the topic standards, individual disclosure requirements were assessed for their materiality in accordance with the materiality assessment process and the information to be reported was selected accordingly. If the materiality was not confirmed, datapoints were omitted.