Key Sites

| Significant Fraport Group airports | ||||||

|---|---|---|---|---|---|---|

| Site | Airport | Company | Share in % | Term | Ownership | |

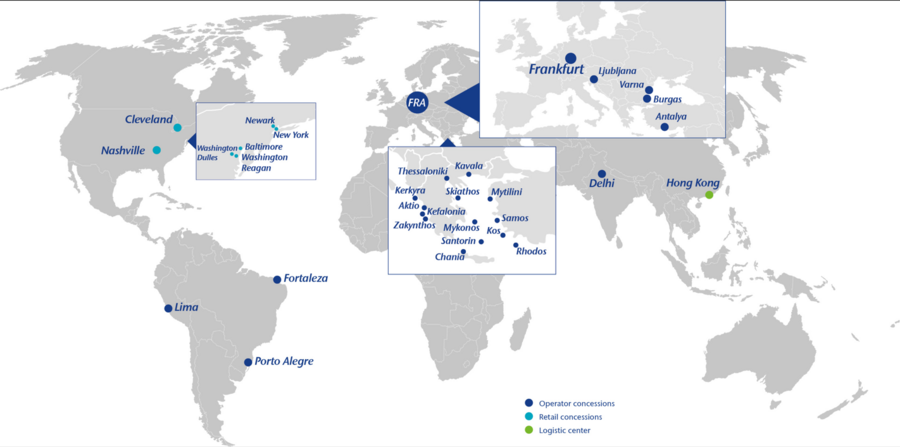

| Germany | Frankfurt | Fraport AG Frankfurt Airport Services Worldwide | 100 | 1924 | no time limits | – |

| Slovenia | Ljubljana | Fraport Slovenija, d.o.o. | 100 | 2014 | no time limits | – |

| Concession charge | ||||||

| Brazil | Fortaleza | Fraport Brasil S.A. Aeroporto de Fortaleza | 100 | 2017 | 2047 | Fixed minimum + revenue component |

| Porto Alegre | Fraport Brasil S.A. Aeroporto de Porto Alegre | 100 | 2017 | 2042 | ||

| Peru | Lima | Lima Airport Partners S.R.L. | 80.01 | 2001 | 20511) | Fixed minimum+ revenue component |

| Greece | 14 Airports | Fraport Regional Airports of Greece A S.A. | 65 | 2017 | 2057 | Fixed minimum + EBITDA component |

| Fraport Regional Airports of Greece B S.A. (below collectively referred to as Fraport Greece2)) |

65 | 2017 | 2057 | |||

| Bulgaria | Varna | Fraport Twin Star Airport Management AD | 60 | 2006 | 2046 | Fixed minimum + revenue component |

| Burgas | 60 | 2006 | 2046 | |||

| Türkiye | Antalya (FTA I) | Fraport TAV Antalya Terminal İşletmeciliği A.Ş. (hereinafter: Group company Antalya I) |

50/513) | 1999 | 2026 | Fixed amount |

| Antalya (FTA II) | Fraport TAV Antalya Yatirim, Yapim ve İşletme A.Ş (hereinafter: Group company Antalya II) |

50/514) | 2027 | 2051 | Fixed amount | |

1) Including extension option. 2) The Group companies Fraport Regional Airports of Greece A, Fraport Regional Airports of Greece B, and Fraport Regional Airports of Greece Management Company are collectively referred to as “Fraport Greece.” 3) Dividend share: 50%, capital share: 51%. 4) From 2027, dividend share: 50%, capital share: 49%. | ||||||

In addition to the aforementioned airports, Fraport operates retail areas at different airports in the USA through its Group company Fraport USA.

Competitive Position at the Frankfurt Site

Frankfurt Airport competes with other airports both nationally and internationally. Regionally, there is competition for passengers and air freight with airports in the original catchment area. Internationally, Frankfurt Airport competes for domestic and international transfer passengers and transshipment freight on the basis of its function as an international transfer airport. The Lufthansa Group remains the most important customer at the Frankfurt site in the 2024 fiscal year, accounting for 67% of the total seat capacity. The largest competitors for transfer passengers are primarily the hub airports London Heathrow, Paris Charles de Gaulle, Amsterdam Schiphol, Istanbul, and Munich, which are in particular influenced by the global route networks of their resident main customers British Airways, Air France-KLM, Turkish Airlines, and Lufthansa Group. Due to the dynamic development of many airlines and airports from the Middle East, the Frankfurt site is also in intercontinental competition with these airports.

In particular, the expansion and modernization programs contribute to maintaining and improving the international competitive position. Terminal 3 (“Expansion South”) should ensure the long-term landside capacities required to give the site a successful future-oriented competitive edge. Numerous technical installations are running inside the terminal. Piers G and H of Terminal 3 have been completed except for the installations that are required for the start of operations. The parking garage is already available for use and has a capacity of more than 2,000 parking spaces. The main terminal building and Pier J are in the final stages of completion. The opening of the new terminal is planned for after the 2026 Easter holidays.

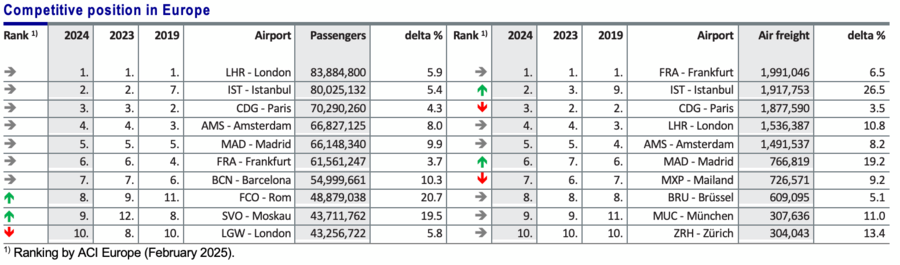

The ranking of the top 10 airports in Europe, which changed during the coronavirus crisis, is returning to the pre-crisis structure (ranking according to ACI Europe; as at: February 2025). With 61.6 million passengers, Frankfurt Airport ranked sixth among the leading airports in terms of passengers in the reporting year. In Germany, Frankfurt Airport was the largest passenger airport, ahead of Munich with 41.6 million passengers in the same period. Based on its air freight turnover of approximately 2.0 million metric tons, Frankfurt has remained Europe’s leading airport in the same period, ahead of Istanbul and Paris Charles de Gaulle.

Competitive Position Outside the Frankfurt Site

The competitive positions of the major airports in the Fraport Group are shown below.

As the airport of the country’s capital, the development of the Group airport in Ljubljana is closely linked to the economic and tourist situation in Slovenia. Competition comes in particular from nearby airports such as Zagreb and Venice. The site is aiming to strengthen its competitive position through continuous capital expenditure in infrastructure and service quality. Most recently, connectivity has been improved by increasing flights to major hubs and resuming flight connections. During the summer months in particular, an increased number of charter flights to holiday destinations around the Mediterranean Sea boosted the appeal of the site.

Passenger numbers at the two Brazilian airports Porto Alegre and Fortaleza are strongly influenced by domestic traffic. The Brazilian aviation market is dominated by the three airlines LATAM Brasil, GOL, and Azul. These airlines also offer numerous connections in Porto Alegre and Fortaleza. The Group airport Porto Alegre benefits from the economically strong Rio Grande do Sul region. In May 2024, however, the airport was considerably affected by severe flooding in the state, which led to a suspension of flight operations for around six months. After reopening with limited operations in October, Porto Alegre Airport resumed full operations in December 2024. Fortaleza Airport is highly tourist-oriented and is conveniently located for flight connections to Europe and North America. Traffic was most recently affected by the airline GOL’s reduction in frequencies at Fortaleza Airport and its discontinuation of certain connections as a result of its Chapter 11 insolvency proceedings.

The Jorge Chávez Airport in Lima is Peru’s leading airport, and one of the largest airports in South America. The site profits from its geographical position, which makes the airport an attractive transfer point for traffic between South and North America. LATAM Airlines Group has the largest share of aircraft movements and passengers at Lima Airport. The largest low-cost airlines at the site, SKY Airline and Jetsmart, continue to pursue a growth strategy and contribute to traffic growth. The expansion program at the airport includes the construction of a new passenger terminal and the now completed second runway, including aprons and taxiways, as well as other peripheral infrastructure. This will ensure that sufficient capacity is available for further growth in the South American aviation market in the future. The inauguration of the new passenger terminal is scheduled for the end of March 2025.

The traffic and business developments at the strongly tourist-oriented Greek sites, at Varna and Burgas, as well as in Antalya are substantially affected by charter traffic of tourist carriers. There is generally no substantial concentration of individual airlines. In addition to the economic development in each respective country where the traffic originates, the sites depend particularly on the appeal of the respective regions with regard to safety, quality, price level, and entry requirements.

Fraport Greece operates 14 Greek regional airports. These are the airports in Kerkyra (Corfu), Chania (Crete), Kefalonia, Kavala, Aktio, Thessaloniki, Zakynthos, Mykonos, Skiathos, Santorini (Thira), Kos, Mytilini (Lesbos), Rhodes, and Samos. Greece’s appeal as a tourism destination and the associated potential for a further increase in demand is expected to grow in the coming years. The positive trend in the traffic figures of previous years continued in 2024.

The Black Sea airports in Burgas and Varna are the second- and third-largest passenger airports, respectively, in Bulgaria after Sofia. In addition to charter services, low-cost transport promises further growth potential. In Varna, Wizz Air provided the largest share of passengers by far, at around 27%. In 2024, the airline temporarily stationed two aircraft in Varna, but reduced this to one aircraft during the year. At the airport in Burgas, meanwhile, Ryanair and Smartwings were on an equal footing, each accounting for 13%. The modular expansion of the terminals at both sites offer sufficient capacity to be able to meet the regional growth expected in the medium term.

Antalya is the third-largest passenger airport in Türkiye behind Istanbul Airport and Istanbul Sabiha Gökçen Airport, and is still one of the most important tourist airports in the Mediterranean Sea region. The demand for holiday travel, which is important for the further development of traffic, is continuously high. It is primarily determined by the political and economic developments in the countries of origin of the main passenger groups as well as Türkiye. At the end of 2021, a consortium made up of Fraport and its Turkish partner TAV was awarded the contract for the new operating concession at Antalya Airport. The operational period of the new concession will start at the beginning of 2027 after the current concession expires, and will run until the end of 2051. As part of the new concession, necessary expansion measures at the terminals and other areas at the airport have been in progress as of the first quarter of 2022. The inauguration of the major infrastructure expansions is expected to take place at the beginning of the second quarter of 2025. The expansion of capacity should ensure that Antalya Airport remains highly competitive in the segment of tourist airports in the Mediterranean region in the long term.

Additional information about business development in the past fiscal year can be found in the “Economic Report” chapter.